The conventional view of Africa as a continent defined by investment risk has always been incomplete, and today it is looking increasingly outdated. While the world’s attention has been consumed by tensions in the Gulf, Ukraine, Taiwan, and by global trade wars, a quieter but significant shift is reshaping Africa’s economic position. Geopolitical fragmentation is transforming the continent into something resembling a seller’s market, not uniformly, and not without genuine difficulties, but in ways compelling to those willing to commit to its multifaceted markets and understand its nuances.

The continent accounts for roughly 3% of global trade and 4% of global foreign direct investment, yet it holds 30% of the world’s mineral reserves, has the world’s youngest and fastest-growing workforce, and sits at the intersection of competing great-power supply-chain strategies. That divergence is driving a reassessment of the continent’s strategic importance.

Africa’s emergence as a strategic negotiator

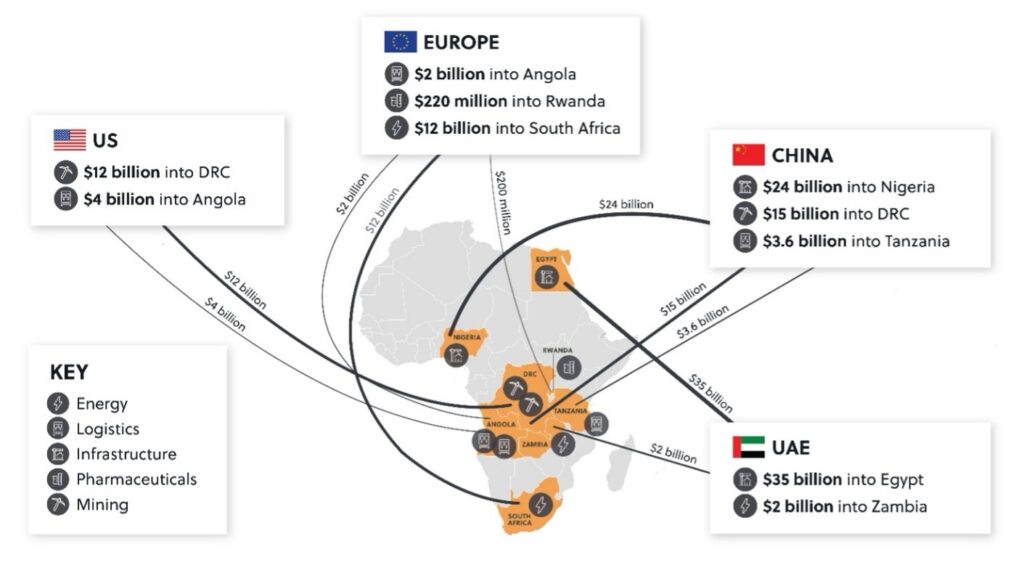

The conventional rules-based trade order is under sustained pressure. As great powers like the United States, China, Europe, and the Gulf compete for access to resources, markets, and geopolitical alignment, African governments find themselves in a stronger negotiating position than at any point in recent decades. China has invested roughly $500 billion in Africa since 2000, with a heavy focus on infrastructure and resource extraction, including nearly $15 billion into mining projects in the DRC alone. The United States has responded with its own strategic commitments, most notably to the Lobito and Liberty Corridors, linking mineral rich hinterlands to Angola and Liberia’s coasts, respectively. The EU is intending to mobilise up to $170 billion in infrastructure investment in Africa by 2027, of which transport corridor investment is a central pillar.

These investments reflect strategic calculations about mineral access, supply-chain security, and geopolitical influence, and African governments are increasingly leveraging great power-competition for these resources to extract better terms – including local processing requirements, technology transfer, and favourable revenue arrangements. It is a posture that echoes the “third path” that Canadian Prime Minister Mark Carney outlined in Davos earlier this year – the argument that middle powers should forge their own course in a world characterised by increasingly self-serving global powers and weakening multilateral institutions.

Who’s investing where and why?

The five sectors benefitting from geopolitical shifts

The leverage African governments are gaining is not just abstract – we are seeing it materialise in concrete opportunities at a sectoral level. The five sectors below are where that dynamic is most legible currently:

Energy. Recurring tensions around the Strait of Hormuz have thrown the vulnerability of global energy supply chains into sharp relief. This has accelerated the conversation amongst energy-importing governments as to how to reduce dependence on supply routed through geopolitically unstable chokepoints. Renewable energy is the most promising long-term answer, and Africa’s endowment positions it as one of the most compelling sources for future supply. Agreements such as the Africa-EU Green Energy Initiative reflect the centrality of Africa to the energy security solutions of global powers, and renewable energy programmes in South Africa, Egypt, Morocco, Ethiopia and Kenya are set to benefit from falling costs for solar, wind and battery storage.

Manufacturing. Morocco has combined geographic proximity to Europe, competitive manufacturing costs, and preferential trade access to attract $5.6 billion in Chinese battery gigafactory investment in 2025, positioning itself to supply components for up to 500,000 electric vehicles annually by late 2026. Morocco already produces one million vehicles per year, and its free-trade agreements with both the US and the EU provide tariff-free access to over one billion consumers. Other candidates for ‘nearshoring’ investment – the practice of ameliorating supply chain vulnerabilities by relocating manufacturing to countries closer to a home market – include Egypt, Kenya, and South Africa. All three countries offer functioning infrastructure, stable trade access, and policy stability, though each comes with its own set of preconditions and complications.

Infrastructure and logistics. Africa’s infrastructure deficit has historically hindered competitiveness, but geopolitical competition has been unlocking the capital to address it. The Lobito Corridor is the most prominent example, but it is not the only one: the Simandou project in Guinea, one of the world’s largest untapped iron ore deposits, and the Nacala corridor in Mozambique are moving forward swiftly. China has also committed $1.4 billion to rehabilitating the Tazara railway linking Zambia to Tanzania, securing an alternative Indian Ocean export route for itself. Corridors offer a catalytic effect to development, in that the infrastructure associated with them can unlock adjacent investment opportunities in agriculture, energy and manufacturing, amongst other sectors. With logistics corridors set to proliferate – the EU has earmarked 12 of them for development – those with awarded operational concessions and diversified financing structures are perceived to be more sustainable than those dependent on a single sponsor.

Pharmaceuticals. The Covid-19 pandemic exposed Africa’s near-total dependence on imported medicines and vaccines, with the continent importing 70–80% of the pharmaceutical products it consumes. The African Union has set a target of manufacturing 60% of Africa’s vaccines domestically by 2040, backed by a $2 billion Afreximbank facility and commitments from the African Development Bank and the World Bank. The regulatory environment is also improving through the African Medicines Agency, launched in 2022, which is beginning to reduce the fragmentation that has historically limited regional market access. South Africa’s Aspen Pharmacare serves a benchmark – a globally competitive generic-drug manufacturer that demonstrates what is possible with accumulated manufacturing capability. The sector requires patient capital, but offers predictable government demand and strategic alignment with continental priorities.

Digital services and fintech. Kenya’s mobile-money ecosystem, anchored by M-Pesa, has become a reference point for digital financial innovation globally, with mobile-money penetration in the country now exceeding 91%. The development of embedded finance, which layers higher value services such as credit, insurance, and savings, on top of already-trusted mobile money infrastructure illustrates how the sector continues to mature. Nigeria, Kenya, South Africa, and Egypt are the leading fintech markets, attracting venture capital across payments, digital lending, SME financing, and Insurtech, many of which are now AI-augmented. Regulatory sandboxes in these jurisdictions has allowed for experimentation that more rigid systems would not permit, and the underlying architecture required for these services – such as undersea cables, data centres and payment rails – have received a surge of investment as capital redirects to Africa in the context of a US-China trade war.

Conclusion

Africa is not a single investment proposition. Morocco’s competitive advantages in nearshoring do not translate to Nigeria, Kenya’s digital infrastructure is not evenly replicated across East Africa, and South Africa’s manufacturing depth coexists with tariff headwinds and structural economic challenges. Approaching the continent therefore requires a framework that assesses sector-specific opportunity with country-specific conditions, such as infrastructure quality, policy stability, trade access, and the regulatory environment. These factors then need to be stress-tested against geopolitical variables, like resource nationalism, the status of great power competition, and the direction of travel of domestic politics. This won’t guarantee returns, but will better inform a risk-reward equation already favourably tilted by the structural pressure driving major powers to compete for access in Africa.